The Stock Market View of AEC: Who’s Public, Who’s Winning, and Why Autodesk Fell Off the Tech Throne

A data-driven look at the publicly traded companies that build, design, and digitize the built environment — and what their valuations say about where the industry is going.

Why this matters

The Architecture, Engineering, and Construction industry is one of the largest sectors of the global economy.

In the United States alone, construction spending reached an annual rate of $2.19 trillion by early 2026, representing roughly 4.4% of U.S. GDP and employing around 8.3 million people.

Yet for an industry of that scale, the number of pure-play AEC companies trading on public exchanges is surprisingly small (and the way their market values have evolved over the last decade tells a story very different from the boom narrative you’d expect).

This post breaks the public AEC universe into three buckets — software vendors, engineering & consulting firms, and contractors & materials suppliers — compares their current valuations and growth, overlays them against U.S. construction activity, and then closes with a hard look at how Autodesk, once among the most valuable software companies in the world, slid out of the top tier.

The publicly traded AEC universe

Software & technology platforms

These are the companies that sell the design, modeling, project management, and digital-twin tools that the industry runs on.

| Company | Ticker | Market Cap (mid-2026) | 1Y Change | IPO / Listed |

|---|---|---|---|---|

| Autodesk | NASDAQ: ADSK | ~$50B | −20% | 1985 |

| Trimble | NASDAQ: TRMB | ~$15.9B | +11% | 1990 |

| Bentley Systems | NASDAQ: BSY | ~$10.1B | −24% | 2020 |

| Nemetschek | ETR: NEM | ~$8.9B | flat | 1999 |

| Procore | NYSE: PCOR | ~$7.1B | −23% | 2021 |

Sources: [^3][^4][^5][^6][^7][^8]

Engineering & consulting firms (the "Big Five")

Five publicly traded consultancies — Jacobs, AECOM, WSP, Stantec, and Tetra Tech — now control 51% of the U.S. environmental & sustainability consulting market, up from 39% in 2019, with combined revenues over $11.3 billion in that segment alone [^9].

| Company | Ticker | Market Cap (mid-2026) | TTM Revenue |

|---|---|---|---|

| Jacobs Solutions | NYSE: J | ~$13.5B | $13.2B |

| AECOM | NYSE: ACM | ~$10.1B | $16.1B |

| Tetra Tech | NASDAQ: TTEK | ~$8B | ~$5.9B |

| WSP Global | TSX: WSP | (Canada-listed) | – |

| Stantec | NYSE: STN | (cross-listed) | – |

Sources: [^10][^11][^12]

Contractors, infrastructure & materials

This is where the largest market caps in the AEC value chain actually live — and where the post-IIJA infrastructure boom shows up most clearly.

| Company | Ticker | Market Cap (mid-2026) | What they do |

|---|---|---|---|

| Quanta Services | NYSE: PWR | ~$84B | Electrical infrastructure |

| Vulcan Materials | NYSE: VMC | ~$38B | Aggregates |

| Martin Marietta | NYSE: MLM | ~$36B | Aggregates & materials |

| Sterling Infrastructure | NASDAQ: STRL | ~$16B | Site dev for data centers, transport |

| United Rentals | NYSE: URI | mega-cap | Equipment rental |

Sources: [^13][^14][^15][^16]

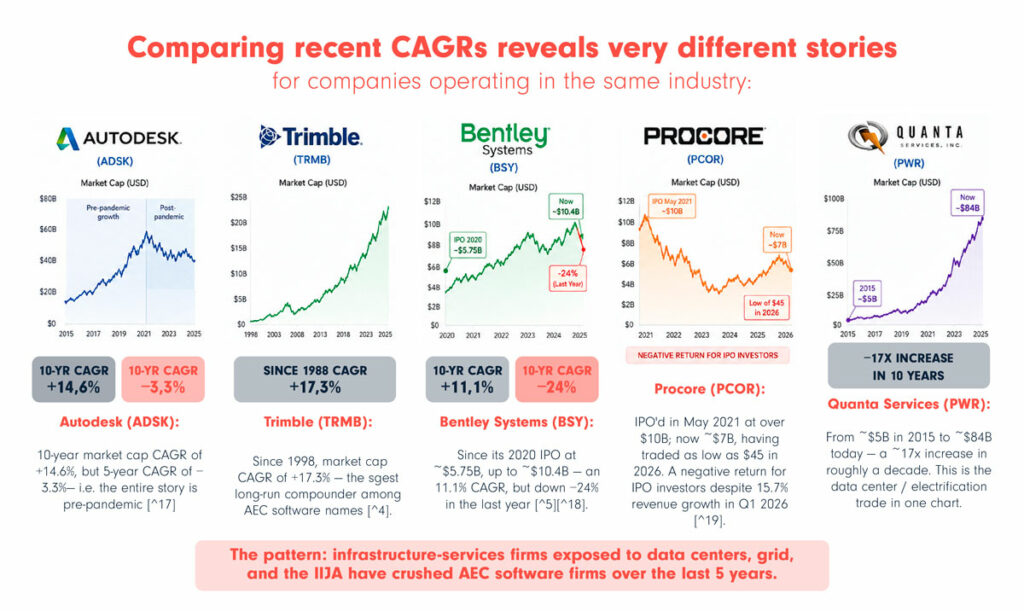

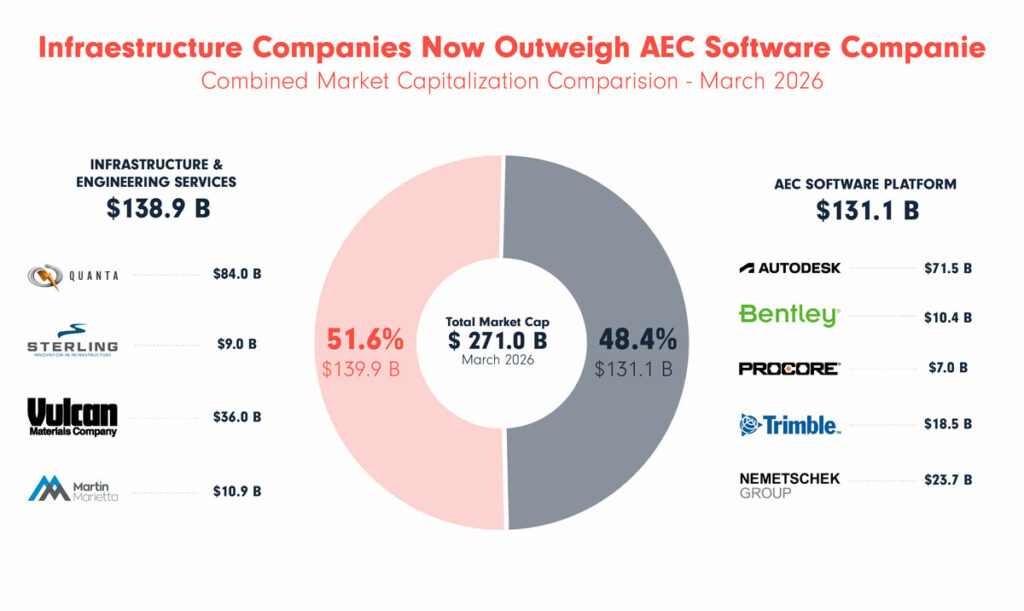

The single most interesting data point in those tables: Quanta Services alone is worth more than Autodesk, Bentley, Nemetschek, and Procore combined.

The boring business of stringing high-voltage lines for data centers and grid modernization has out-valued the entire pure-play AEC software stack.

This is a trend that is completely opposite to other industries where software companies end up with higher valuations compare to traditional companies.

Growth trajectories: who's actually winning

Overlay: AEC stocks vs. U.S. construction spending

U.S. construction spending crossed $2 trillion in annualized run-rate for the first time in 2022 and has hovered between $2.1T and $2.2T since.

December 2025 closed at $2,168.8B, and March 2026 estimates put the SAAR at $2,185.5B — about 1.6% above March 2025 [^1][^20].

Full-year 2025 construction spending actually fell −1.4% YoY, marking the first annual contraction since 2020 [^20].

Key context for interpreting AEC stocks against that backdrop:

- Private nonresidential construction declined −3.1% in 2025 — the segment that drives commercial design fees, BIM software seats, and contractor backlogs [^20].

- Public construction rose, with highway spending surging +3.3% in early 2026 thanks to IIJA disbursements [^21].

- The IIJA and Inflation Reduction Act are injecting over $580 billion into the AEC industry between 2022 and 2026 [^22].

This split explains why share prices have diverged so sharply.

Companies tied to public infrastructure and electrification (Quanta, Sterling, Vulcan, Martin Marietta) ride the public-spending wave.

Companies tied to commercial real estate, private design budgets, and SaaS seat growth (Autodesk, Bentley, Procore, Nemetschek) feel every commercial slowdown immediately — and have absorbed a separate, AI-related shock in 2025–2026.

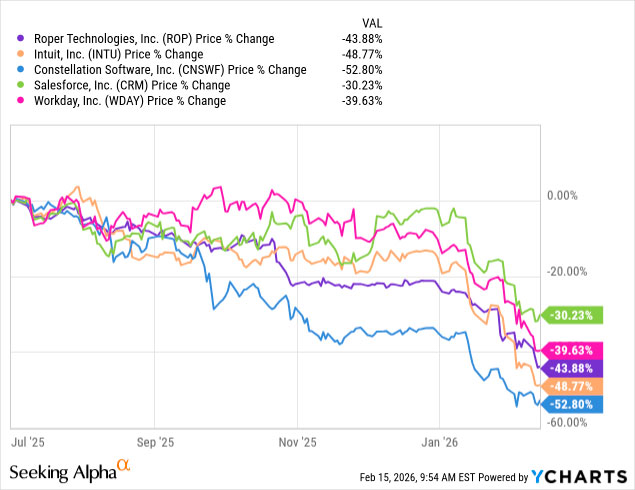

The AI fear that hit engineering stocks

In late 2025 and into 2026, a thesis spread across capital markets: AI will commoditize the high-margin work that engineering and design consultancies charge premium fees for.

Since the thesis took hold roughly six months before this writing, Stantec is down ~23.7%, WSP down ~23.1%, while the broader Canadian index (S&P/TSX Composite) was up 12.5% over the same period [^23].

In the U.S., Jacobs, AECOM, and Tetra Tech have all sold off in tandem [^23]. The same fear has weighed on Autodesk, Bentley, and Procore — all of which now trade well off their 2024 highs despite reporting solid revenue growth.

Whether that fear is correct is a separate debate. (At e-verse we’ve argued AI is not yet meaningfully disrupting AEC design workflows.) But it’s priced in, and it has reshaped how the market values everything in this industry.

The Autodesk story: from tech titan to also-ran

In December 1998, Autodesk’s market cap was $1.75 billion [^17].

The company had pioneered CAD on the PC with AutoCAD (1982), gone public on NASDAQ in 1985, and by 1989 owned ~60% of the PC CAD market with $117 million in revenue [^24][^25].

Through the 1990s, Autodesk was routinely on lists of the largest U.S. software companies, alongside Microsoft, Oracle, Lotus, and Adobe.

Its 2002 acquisition of Revit Technology Corporation for $133 million [^26] reshaped the architecture industry.

Autodesk peaked on August 25, 2021, at $342.27/share with a market cap of roughly $70 billion [^27].

That valuation reflected near-perfect conditions: a finished subscription transition, COVID-era SaaS multiple expansion, and exuberance about Forma, Tandem, and the construction cloud stack.

Today, Autodesk’s market cap sits around $50 billion — meaningful, but a ~30% drawdown from peak. More importantly, look at where that places Autodesk on the global software leaderboard.

The current Top 10 software companies by market cap (2026), per the Forbes Global 2000 ranking:

- Microsoft — ~$3.11T

- Alphabet — ~$2.5T+

- Meta — ~$1.55T

- Oracle — ~$552B

- Palantir — ~$314B

- SAP — ~$324B

- Salesforce — ~$257B

- ServiceNow — ~$196B

- Intuit — ~$174B

- Adobe — ~$157B

[^28]

Autodesk, at $50B, ranks roughly #446 globally by market cap, well outside the top ten software companies, and below pure-play SaaS names like Workday, HubSpot, Cadence, and Datadog [^29].

The Forbes ranking that did include Autodesk among the top 25 software companies in March 2024 [^30] would no longer place it there today.

What changed?

Several forces compounded:

1 – The software stack got specialized. Salesforce ate CRM. ServiceNow ate ITSM. Snowflake and Databricks ate the data layer. Each of those addressable markets turned out to be much larger than CAD/BIM — and each had buyers writing far bigger checks than architects do.

2 – AEC is structurally smaller and more fragmented than horizontal SaaS. The entire global AEC software market is forecast at just $12.04 billion in 2026, reaching $17.98 billion by 2031 at an 8.35% CAGR [^31]. That ceiling caps how big any pure-play AEC vendor can get. A horizontal CRM platform faces no such ceiling.

3 – Competitors have eroded the monopoly. Bentley dominates civil infrastructure. Nemetschek’s Allplan, Vectorworks, and Bluebeam have held verticals. Procore took the construction-management war. Trimble bought Tekla in 2011 and made structural a real fight. Even ZWSOFT and BricsCAD now compete credibly on AutoCAD’s home turf.

4 – The subscription transition consumed a decade. From roughly 2016 to 2023, Autodesk poured strategic oxygen into the painful (but ultimately correct) shift from perpetual licenses to subscription. While that played out, Adobe finished the same transition cleanly and pulled ahead by a full order of magnitude.

5 – AEC clients don’t pay like enterprise IT. A typical mid-sized architecture firm spends a small fraction of its revenue on software, compared with the 10%+ that financial services or healthcare firms route to enterprise platforms. The TAM is real, but it’s low velocity.

The lesson isn’t that Autodesk has failed — its TTM revenue of $7.21 billion and net income of $1.12 billion make it a strong business [^32]. The lesson is that being the dominant software company in AEC is no longer a path to being a top-tier technology company. The asymmetry between horizontal SaaS and vertical AEC SaaS has widened to a chasm.

What this means for the next five years

A few signals worth tracking:

- The center of gravity in AEC public markets has moved from software to infrastructure services. As long as data center, electrification, and IIJA spending continues, Quanta, Sterling, Vulcan, and Martin Marietta will remain the largest pure-play AEC stocks by market cap.

- AI will continue to compress valuations of design-fee businesses until either the productivity gains show up in margins (bull case) or the fee compression shows up in revenue (bear case). The market is currently pricing the bear case.

- Pure-play AEC software is a difficult home for venture capital. With the entire global TAM under $18B by 2031, very few startups can return a billion-dollar fund. Expect more consolidation: Bentley has already done 25 acquisitions since its 2020 IPO, spending over $2.3 billion [^33].

- The data center build-out is the single biggest AEC story of the decade. Sterling’s data-center-exposed E-Infrastructure segment alone generated $1.47 billion in 2025, up 59% YoY [^15]. Any AEC software vendor that solves real problems for hyperscalers will have outsized opportunity.

For services firms — like e-verse — operating at the boundary between software and AEC, the takeaway is that the value chain has reorganized around infrastructure and AI, not around traditional design. Following the capital is, as always, the clearest signal of where the industry is going.

Sources

[^1]: U.S. Census Bureau, Monthly Construction Spending, March 2026 (released May 7, 2026). https://www.census.gov/construction/c30/pdf/release.pdf

[^2]: Construction Coverage, U.S. Construction Market Size & Industry Data (May 2026). https://constructioncoverage.com/data/us-construction-spending

[^3]: MacroTrends, Autodesk Market Cap 2012–2026 (ADSK). https://www.macrotrends.net/stocks/charts/ADSK/autodesk/market-cap

[^4]: StockAnalysis, Trimble Market Cap & Net Worth (TRMB). https://stockanalysis.com/stocks/trmb/market-cap/

[^5]: StockAnalysis, Bentley Systems Market Cap & Net Worth (BSY). https://stockanalysis.com/stocks/bsy/market-cap/

[^6]: CompaniesMarketCap, Nemetschek (NEM.F). https://companiesmarketcap.com/nemetschek/marketcap/

[^7]: MacroTrends, Procore Technologies Market Cap 2019–2026 (PCOR). https://www.macrotrends.net/stocks/charts/PCOR/procore-technologies/market-cap

[^8]: Investing.com, Procore Technologies Stock Price (May 2026). https://www.investing.com/equities/procore-technologies

[^9]: Environment Analyst Global, US E&S Consulting Sees ‘Big Five’ Increase Dominance (June 2025). https://environment-analyst.com/global/110992/us-es-consulting-sees-big-five-increase-dominance

[^10]: PitchBook, Jacobs Solutions Company Profile (May 2026). https://pitchbook.com/profiles/company/41254-21

[^11]: Wikipedia, AECOM (FY2025 financials). https://en.wikipedia.org/wiki/AECOM

[^12]: Yahoo Finance, AECOM (ACM) Quote. https://finance.yahoo.com/quote/ACM/

[^13]: CompaniesMarketCap, Quanta Services (PWR). https://companiesmarketcap.com/quanta-services/marketcap/

[^14]: Investing.com, Vulcan Materials (VMC). https://www.investing.com/equities/vulcan-matrls

[^15]: Sterling Infrastructure 8-K filing, Q1 2026. https://www.sec.gov/Archives/edgar/data/0000874238/000087423826000052/q12026earningsreleaseppp.htm

[^16]: Motley Fool, Best Construction Stocks for 2026. https://www.fool.com/investing/stock-market/market-sectors/industrials/construction-stocks/

[^17]: StockAnalysis, Autodesk Market Cap & Net Worth (ADSK). https://stockanalysis.com/stocks/adsk/market-cap/

[^18]: Bentley Systems IPO data via PitchBook. https://pitchbook.com/profiles/company/40628-80

[^19]: Investing.com, Procore Q1 2026 Earnings (May 2026). https://www.investing.com/equities/procore-technologies

[^20]: MTS Insights / U.S. Census Bureau, US Construction Spending (full-year 2025 and Jan/Feb 2026 releases). https://www.mtsinsights.com/events/4385/

[^21]: Trading Economics, United States Construction Spending (Jan 2026 release). https://tradingeconomics.com/united-states/construction-spending

[^22]: Cascade Partners, AEC Industry Market Update (Feb 2026). https://cascade-partners.com/aec-industry-market-update/

[^23]: The Globe and Mail, AI Fears Sink Stantec and WSP Shares (May 2026). https://www.theglobeandmail.com/business/article-ai-fears-sink-stantec-and-wsp-shares-turning-the-high-flying/

[^24]: Funding Universe, History of Autodesk, Inc. https://www.fundinguniverse.com/company-histories/autodesk-inc-history/

[^25]: Wikipedia, Autodesk. https://en.wikipedia.org/wiki/Autodesk

[^26]: MatrixBCG, Brief History of Autodesk. https://matrixbcg.com/blogs/brief-history/autodesk

[^27]: CompaniesMarketCap, Autodesk Stock Price History. https://companiesmarketcap.com/autodesk/stock-price-history/

[^28]: Wikipedia, List of the Largest Software Companies (Forbes Global 2000, 2025 data). https://en.wikipedia.org/wiki/List_of_the_largest_software_companies

[^29]: FinanceCharts, Autodesk (ADSK) Market Cap History. https://www.financecharts.com/stocks/ADSK/summary/market-cap

[^30]: Yahoo Finance / Insider Monkey, 25 Biggest Software Companies in the US (March 2024). https://finance.yahoo.com/news/25-biggest-software-companies-us-123520322.html

[^31]: Mordor Intelligence, AEC Software Market Size, Share, Trends 2031 (Jan 2026). https://www.mordorintelligence.com/industry-reports/aec-software-market

[^32]: PitchBook, Autodesk Company Profile (April 2026). https://pitchbook.com/profiles/company/25163-02

[^33]: AEC Technology Guy Substack, Bentley Systems: From a Little Company to a Big Vision (March 2025). https://aectechnologyguy.substack.com/p/bentley-systems-from-a-little-company

Valentin Noves

I'm a versatile leader with broad exposure to projects and procedures and an in-depth understanding of technology services/product development. I have a tremendous passion for working in teams driven to provide remarkable software development services that disrupt the status quo. I am a creative problem solver who is equally comfortable rolling up my sleeves or leading teams with a make-it-happen attitude.