After the hype: NFTs and the AEC

Introduction

We’ve previously discussed the impact of the metaverse on the AEC industry, where we introduced some thoughts about the industry and its relationship with the Web3 space.

Can we successfully convert a BIM model at a given stage into an NFT? And, most importantly, is it even worth it?

Here, we’ll look at another piece of the blockchain space: NFTs and the underlying technology that supports them. We’ll dig deeper into what this means for the AEC space and the implications on legal property ownership in both digital and physical environments.

The concept(s)

Let’s start by defining what an NFT is. We must start with the basics and quickly define blockchains, blockchain networks, smart contracts, and tokens.

Please note I’m an enthusiast in the subject, not an expert. Definitions aren’t the primary goal here. The idea is to briefly review the concepts to provide context when we relate them to the AEC industry, as there is a lot of content on the internet already.

Blocks and Blockchains

Bitcoin was the first network to use this technology to support a digital currency network. Managing peer-to-peer transactions without the need to trust the other party (zero-trust architecture), with no third party involved to verify them, was a groundbreaking achievement never seen before, at least successfully.

A couple of years later, Ethereum was born, integrating the ability to execute smart contracts on top of blockchain technology with the same decentralized concepts behind it, becoming not only a network to execute transactions between peers but also a platform to run other applications on top of. But we’ll go deeper into that later.

Many are familiar with the concept of databases. Blockchains are databases with a particular structure: a chain of blocks. Every block is a “package” of data, for example, transaction information. By design, blockchains have the particular quality of being encapsulated and isolated from anything outside the blockchain.

We’ll play with a website that lets us mimic a blockchain in our browser to show what this means quickly [6].

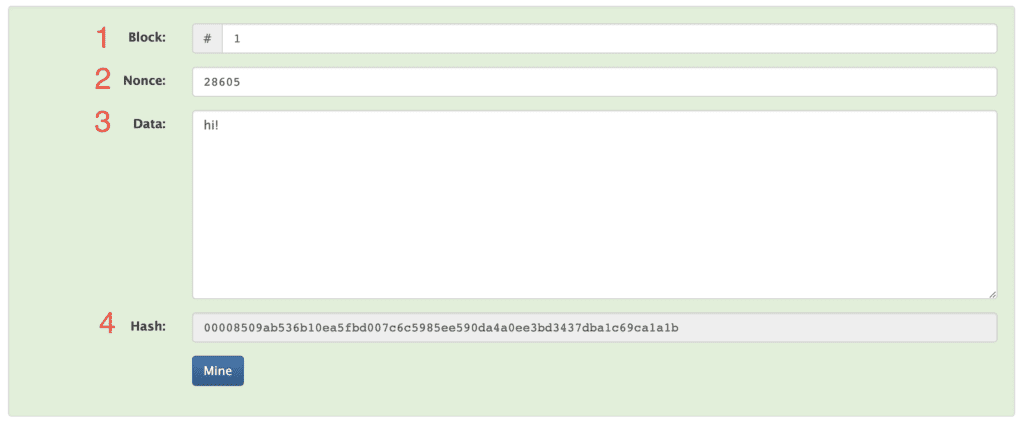

Here, we can see the basic structure of a block:

- Block number: the number of the block in the chain. In this case, this is the first block, usually called the “Genesis Block”.

- Nonce: this is a random number that peers in the network look for that makes the hash (see point 4) match the mining rules in a Proof of Work blockchain, in this case, to find a hash that starts with four zeros. The difficulty of the problem can be adjusted. The critical thing to know is that doing this is computationally intensive.

- Data: the data that the block includes. For example, transaction data would go here, but it can be any data we want. In this case, we just have a word.

- Hash: this is a text result of passing all the data in the three previous fields through a one-way hashing algorithm. It will always be the same length regardless of the input size (it doesn’t matter whether we’re hashing a single word or text from an entire library of books) and look like random characters. The key is that the same data will always produce the same hash, and no two inputs produce the same output. So, anything we change will change the hash, and if we put it back as it was, it will produce the same old hash again.

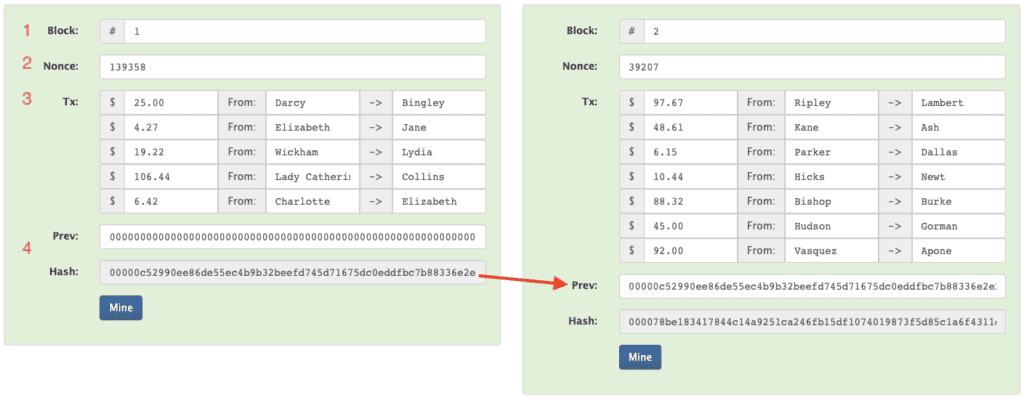

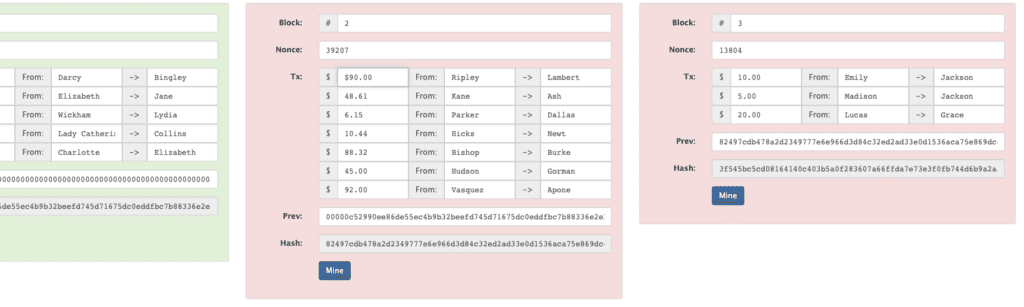

The hash discussed above is a crucial component that chains blocks together. So, in a more “realistic” example of two blocks in a blockchain, we would see something like this:

Points 1, 2, 3 (with transactions as the data instead of a single “hi”), and 4 are the same as explained previously. But, as you can see here, blocks have a “Prev” field that stores the previous block’s hash. For block #1, this is 0000… since it’s our Genesis Block. Block #2 stores block #1’s hash and includes it in the data that produces its hash. Block #3 will store block #2’s hash, doing the same, and so on.

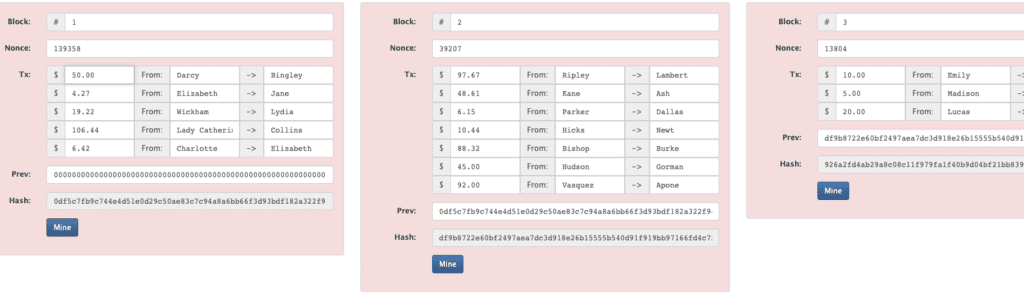

So, what happens if I’m a malicious actor and want to change data in a previous block? For example, in block #1’s first transaction, I want to say that Darcy sent Bingley $50 instead of $25:

Then, all my previous nonces stop producing hashes with four leading zeros, breaking the whole blockchain. If I put things as they were, did this with a block different than #1, and changed a transaction in block #2, something similar would happen to all blocks starting on block #2:

I would have to re-mine all blocks to find nonces that, hashed with the new data plus the previous block’s new hash, produce an output that starts with four zeros… before anyone notices. Lots of work.

Blockchain Networks

The idea here is that besides our single example chain, there are other “peers” with copies of the chain, with all blocks, data, and transactions. Everything is transparent, viewable, and verifiable by anyone. So, here’s where decentralization comes in. These peers fight to find the correct nonce that produces the hash matching the chain’s rules for the next block. The first one to find it sends the result for the other peers to validate.

Finding it can take a long time and lots of work, but validating represents no effort. This is where all the other peers accept the result and add the new block to the chain. Whoever does this first gets the block reward [5]: an amount in the network’s native coin that is emitted (or minted) at that moment that the winner gets to keep. For example, this is how new bitcoins are created until there are no more block rewards, several halvings [7] from now. But that’s for another article.

Changing old blocks was a significant effort in our single-chain example. Imagine a world with millions of peers having copies of the chain. An effort to change anything would be pointless since it’s practically impossible.

This is a basic explanation of the mining or Proof of Work [8] process. We will also not go into Proof of Stake [9]. As mentioned, the idea is not to go too deep into the basic concepts, only enough to provide some context. If you want to look at a more extensive demo on the concept of Blockchains, this fantastic video by the creator of the website we used explains it:

Feel free to play with the live examples of Hash, Block, Blockchain, Distributed Blockchain, and others on this website.

Smart Contracts

Algorithms that run without the need of a person or organization to maintain them in a server, locally, or on top of cloud infrastructure (like AWS) are called decentralized. Smart Contracts fall into this category, as they’re instructions executed without needing a centralized or third-party intermediary to run or verify them. They are sustained by a global community of equal peers running the network.

These are hosted in the blockchain’s blocks, as part of the data they hold, in networks that support this type of functionality (like Ethereum or Solana). As you may remember, the networks are composed of multiple peers with their own copies of the blockchain. For the examples in this article, we’ll focus on Ethereum.

These algorithms are one of the main differences between Ethereum and Bitcoin. Following what you read in the previous section, you probably already understand that once deployed (or, in other words, sent to the network), these are immutable and will live forever on the blockchain. They have an address, like the one you get when you create a wallet in Ethereum, Bitcoin, or other crypto networks.

Anyone can interact with them, like you would interact with an API, as long as they have enough gas (funds) to run. You load ETH on them to make sure they keep running. This is designed to prevent people from hosting smart contracts permanently running, forever, for free, making the whole thing hard to sustain.

Also, for sake of transparency, many of them have their source code published on Etherscan, a site that essentially allows you to search for anything in the Ethereum blockchain.

For example, this is a smart contract I deployed that stores someone’s favorite number, along with their name, and allows you to then read off that list in an Ethereum test network (pretty useless, but enough to illustrate):

/**

*Submitted for verification at Etherscan.io on 2022-10-10

*/

// SPDX-License-Identifier: MIT

pragma solidity ^0.8.8;

contract SimpleStorage {

People[] public people;

uint256 favoriteNumber;

mapping(string => uint256) public nameToFavoriteNumber;

struct People {

uint256 favoriteNumber;

string name;

}

function store(uint256 _favoriteNumber) public virtual {

favoriteNumber = _favoriteNumber;

}

function retrieve() public view returns (uint256) {

return favoriteNumber;

}

function AddPerson(string memory _name, uint256 _favoriteNumber) public {

people.push(People(_favoriteNumber, _name));

nameToFavoriteNumber[_name] = _favoriteNumber;

}

}

This is how it looks on Etherscan. You can see the code and the transactions that interacted with it, including the one that created it.

Tokens

We previously mentioned blockchains usually have their native coin and briefly discussed how these are created. Now, with smart contract functionality, I could create an app deployed on Ethereum that emits its coins for different purposes, actually, any purpose I want.

In this case, these are usually called Tokens [10]. Examples are UNI, RSR, LINK, and thousands of others. These live in the Ethereum blockchain (or the blockchain where the smart contract was deployed) and don’t have their own network. They follow a standard framework called ERC-20 [15] and can represent virtually anything (real-world assets, digital currencies, national currencies, property, financial assets, a measure of gold, etc.).

The examples we have gone through so far are of coins, or tokens, that can be minted to create new units of each, like with the US Dollar or any other national fiat currency.

Non-Fungible Tokens (NFTs)

So, how do NFTs tie to all these concepts?

We already established that some coins and tokens could be minted. New units can be created. This means they are fungible: interchangeable and of the same value. Essentially, they are equal to each other.

But, other tokens are non-fungible: they’re unique, impossible to copy, or for other units to be minted. These are what is famously known as NFTs. And, since they’re still tokens, ownership is easily verifiable, immutable, and easily transferrable at a relatively low cost in a permissionless way, meaning we don’t need to wait for anything or anyone to authorize to transfer or manage an asset that is ours as proven by the blockchain itself in a completely transparent way. All transactions are public.

We mentioned that smart contracts run in blockchains like Ethereum and saw a simple example. But other smart contracts take care of more complex tasks, like emitting NFTs, storing, or allowing them to be interchanged. For example, the entire OpenSea smart contract functionality! Take a look here. This is where OpenSea hosts their smart contract code, allowing its platform’s functionality to mint, transfer, and interact with NFTs.

There’s even a standard framework for creating and issuing NFTs in Ethereum called ERC-721 [12]. If a smart contract implements that standard, it can be called an ERC-721 Non-Fungible Token Contract and will be responsible for emitting and keeping track of the NFTs it creates. For example, here, we can see a list of the top NFT tokens in Ethereum by transfer volume.

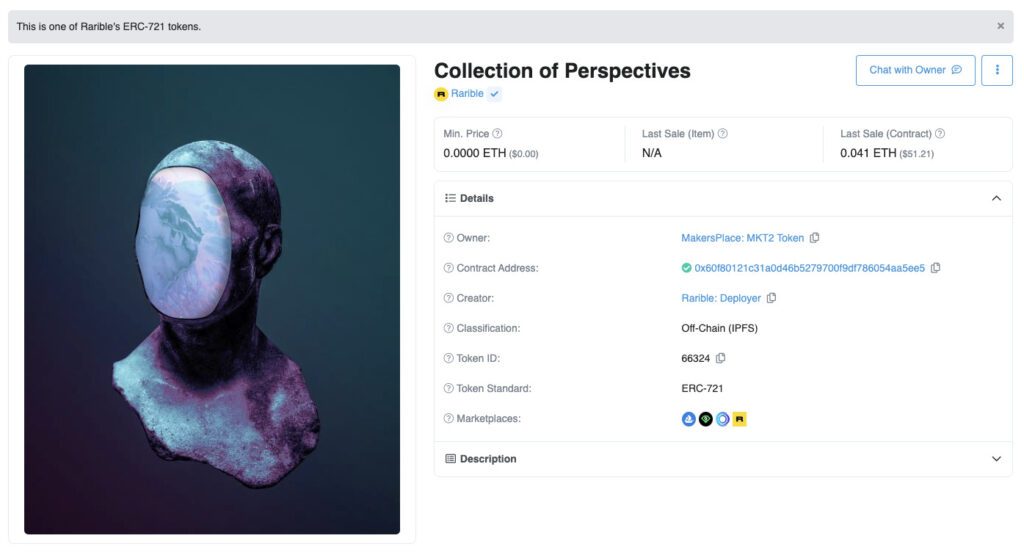

If we look at the basic structure of an NFT, this is an example of what we get:

We can see the following:

- Owner: the wallet that owns the unique token.

- Contract Address: address to the contract that keeps track of the token.

- Creator: the address that deployed the NFT.

- Classification: this establishes if the NFT is stored on or off-chain. Important for our topic today (read ahead!).

- Token ID: the unique identification of the NFT. This is a crucial difference from fungible tokens.

- Standard: the structure that this NFT implements.

- Marketplaces: where it’s traded.

NFT Metadata Storage

An important point to remember is that these tokens point to an asset that can be stored on-chain or off-chain. A work of art NFT will be a token that exists in the blockchain and will have a pointer to the asset it represents as metadata (an image, for example). The metadata here is vital since it will describe the NFT’s unique traits, a description, and where the digital copy is stored.

If this asset is stored in the blockchain (on-chain), the actual file raw data will exist, written and stored in Ethereum in a decentralized way. So, the NFT’s smart contract creates, describes, and stores the token’s asset. This is expensive, especially if we’re dealing with a big file since Ethereum isn’t designed to store large amounts of binary data. For example, storing 1GB of data on-chain at the time of writing, with an ETH price of around $1249 and current gas prices, would cost around 17920 ETH… or about $22 million!

So, most NFTs are stored off-chain. This means the purpose of the token stored in the blockchain is to point to an asset stored elsewhere: servers and storage solutions like AWS S3, Google Cloud, Azure, or even something like Google Drive. In this case, technically, your NFT redirects to a centralized server. If the file it points to were deleted from that centralized server, your NFT would be worthless as it would be directing to nothing.

Luckily, there’s a better off-chain alternative: IPFS (InterPlanetary File System). In theory, it’s a decentralized peer-to-peer (p2p) storage network. This means every user in the network can access and host parts of the data that exists in the network cheaply and securely, a similar concept to torrents and old p2p file sharing systems, eliminating the risk of using centralized solutions where a given user or organization can decide to delete our files.

Although much better, this is not ideal since you’re risking a disruption with the off-chain storage system that could render the link provided by the smart contract useless. In plain English, you’re losing the “immutability” features a blockchain network provides by storing your file outside of it. Anyhow, it’s proven reliable and sustains millions of applications and use cases nowadays, being the backbone of the Web3 ecosystem.

The hype

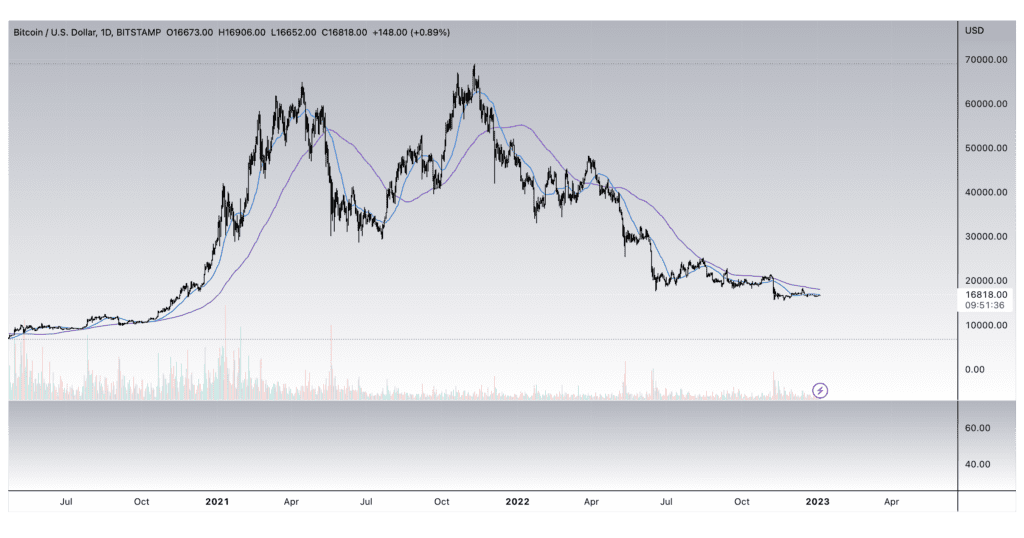

As you may know, there was a gigantic fever around NFTs during the last crypto bull market.

To put things in context, that bull market started in the final days of 2020 and lasted for most of 2021, taking bitcoin to an all-time-high (ATH) price of around $69045 [1] and Ether (Ethereum’s native coin) to $4878 [2], both peaking in November of the same year.

In both cases, we’re down about 75% from the highs at the time of writing, measured in USD pairs.

One of the big narratives in the last bull market cycle was NFTs. During the craziness of the highs, NFT transactions and adoption skyrocketed. The popularity of some NFT collections soared and reached broad markets, with many celebrities like Jimmy Fallon or Eminem acquiring NFTs from the Bored Ape Yacht Club [13] collection. One NFT named Everydays: the First 5000 Days [14] by an artist called Beeple was sold for a record-breaking $69 million at Christie’s, one of the world’s most famous auction houses.

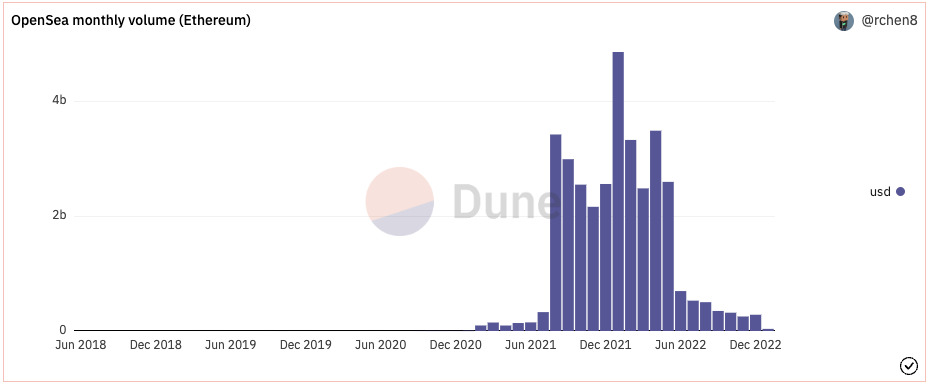

We can see the market frenzy in data from the OpenSea platform [3], one of the best-known NFT marketplaces:

As seen here, the monthly value of traded NFTs in the Ethereum network, measured in USD, peaked shortly after the overall crypto bull market did, decreasing considerably after that.

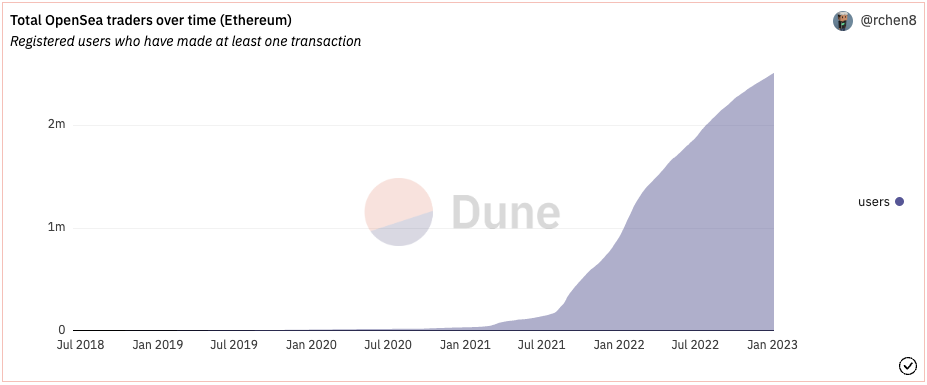

But does this mean actual usage decreased? If we look at the number of people making transactions on the OpenSea platform, that is not the case:

But, OpenSea is just one of the NFT marketplaces out there. There are others, and also other Smart Contract-enabled blockchain networks like Solana. The biggest one is Ethereum.

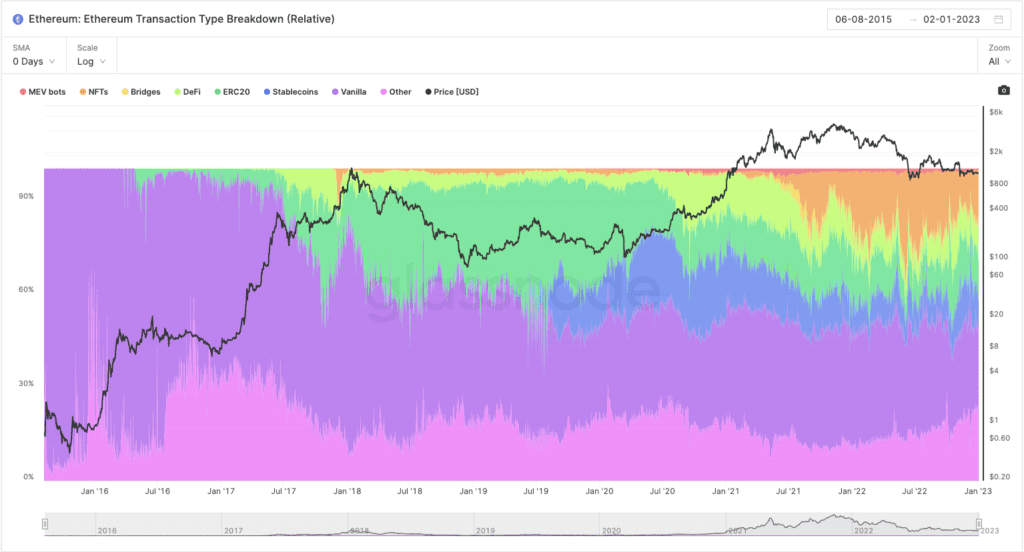

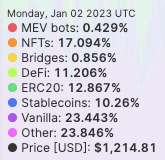

So, let’s take a look at the Ethereum network as a whole in this transaction type breakdown metric provided by Glassnode [4]:

Here, we can see all the different transaction types that the Ethereum network supports and the percentage they represent in the total amount of transactions that exist for all the use cases the network supports. In May 2021, transactions related to NFTs started to grow (the orange section of the graphic) above.

This tendency doesn’t seem to have stopped, with NFTs representing about 17% of all Ethereum transaction usage at the time of writing. To compare, Stablecoins represent around 10% and Vanilla ones about 23% (generic Ether transactions). See the full breakdown here:

This means NFTs have grown to represent an immense portion of transactions in the Ethereum network and a significant use case for smart contract technology in general, at least in user adoption, even after the speculative frenzy plummeted.

Implications for the AEC industry

Now that we understand the basics, we can analyze what this means for our space.

There’s a tendency nowadays to try to force blockchain concepts into everything, regardless of value added. Maybe it’s marketing-friendly? Let’s take a look.

Art and Design

Some companies and individuals in the space have been experimenting with NFTs. We mentioned The Mars House from 2020 by an artist named Krista Kim was the first digital home to be sold as an NFT for about $512000 [16] in a previous article.

Zaha Hadid Architects also experimented with the technology, creating a digital art gallery showcasing different NFTs as an exposition called “NFTism” at Art Basel in Miami [17]:

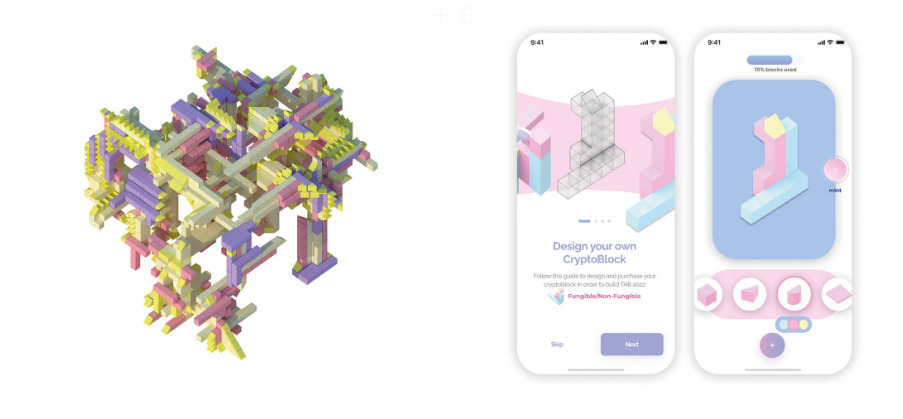

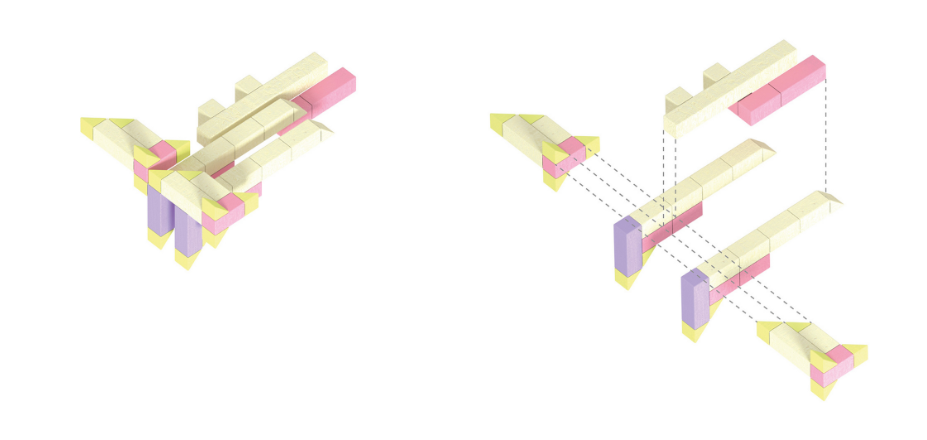

The architectural design studio iheartblob proposed a blockchain-funded pavilion [21] for the Tallinn Architecture Biennale called “Fungible Non-Fungible Pavilion”. An NFT generative tool with a setup that allows individuals to design and mint their own objects, following a set of constraints inside a grid system, interlocking modular components, and made of timber. Every NFT minted by the users funds a physical replica used in the pavilion.

This way, the architects had more of a “system designer” role, creating a structure for users to build on top of:

Projects like these leverage the “artistic” side of NFTs. The digital world can be a massive playground for architects. Experimentation on steroids, without the need to constrain ourselves to real-world limitations like regulations or even gravity, at a low cost, high speed, and without burning resources. With user interfaces in AR/VR quickly improving, these experiences will reach a broader audience, potentially leveling up the design industry in ways we haven’t yet seen.

Leveraging NFTs, creators can profit from their designs when they sell them but can keep “copyright” control on the blockchain and even code their own terms in the NFTs they produce. For example, allowing them to profit every time they are sold on a marketplace, getting a cut each time they are transferred.

Ownership

Another fundamental side to NFTs that is key to our industry is ownership. As we’ve seen, NFTs are an extraordinarily efficient and resilient solution to prove ownership of an asset or transfer it without a public or private entity needing to verify it cheaply and transparently.

Building assets are unique, similar to NFTs. The systems and organizations that manage land management, construction, and real estate ownership are generally inefficient, bureaucratic, and expensive to deal with.

A blockchain governs real-world ownership in a world where NFTs represent land, houses, apartments, and all other buildings. Selling and transferring property to anyone worldwide would take a matter of hours at a small fraction of the current cost. Just pay for the gas fees!

It doesn’t stop there. Currently, many token projects get funding from an ICO (Initial Coin Offering), the crypto industry alternative to an IPO in traditional finance. A real estate developer could finance their projects this way: the building would be a set of NFTs minted and sold to future owners to represent their ownership of the future apartments. Crowdfunding? No problem. NFTs support fractional ownership, so many owners could bid and contribute to funding for a single asset.

The designs for these buildings and all their associated systems could be minted as NFTs, too, for Architects, Designers, and other AEC professionals to get ownership of their ideas and deliverables and better compensation for them.

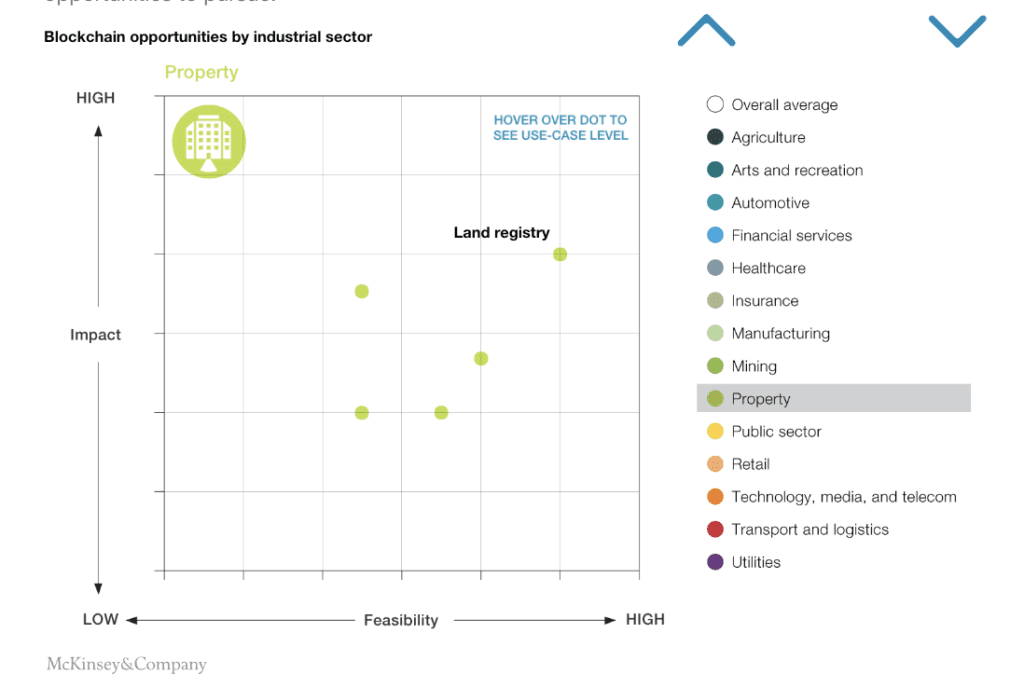

In a McKinsey report about blockchain back from 2018 [19], land registry and other property-related use cases was one of the highest impact, highest feasibility use cases:

Other considered use cases in the report were fractional investing, title exchange, or property leasing. For the full report, visit this link or the references at the bottom.

Governance

Suppose we want to go a step further. In that case, the whole administration of a building could be done in an efficient, decentralized, and transparent way through a DAO (Decentralized Autonomous Organization) [18], a concept allowed by a combination of the technologies mentioned in this article. In our hypothetical example, every owner has a stake in the assets transparently recorded in the blockchain. They could vote accordingly in a coordinated way for decisions being made in their community through such type of organization, eliminating bureaucracy, added cost, inefficiency, and even corruption.

As you may see, NFTs could affect most of the D’s in BIM – from 3D to 7D. And, as we saw, they’re only one of the concepts enabled by smart contracts.

Digital Twins and Supply Chains

The feasibility of turning digital twins of real-world assets into NFTs is high due to their virtual nature. Opportunities arise in commoditizing these digital twins as unique snapshots of a project or operative building at a given stage for use cases that range from the more “artistic” to the operative. For example, trading and reusing design ideas across projects and owners or tracking a project’s progress transparently and reliably, tying unique tokens to BIM assets stored off-chain.

“Master” Digital Twins could be a “main” NFT, with the different levels and assets inside the building being NFTs themselves [20], with different owners, providing secure ownership of a building’s physical and virtual assets.

Suppose we tie digital twins to supply chains. In that case, exciting use cases appear, like tracking networks of contractors and providers for components of project sectors that can be treated as unique assets, with traceability of different products across manufacturing and building stages, on and off-site, achieved by turning these products into tokens.

Carbon credits are another huge topic subject to tokenization, but it makes more sense for them to be fungible tokens instead of NFTs since they all share the same value and properties.

Conclusions

After the hype vanished in terms of market speculation, it’s clearer to see NFT technology poses exciting opportunities for innovation in the AEC sector that go deeper than the trendy, artistic side, leveraging the value they offer in transparency, uniqueness, and ease of transfer. It’s still early to say how deeply it will impact the space, but there’s a pretty good case to be made that we can leverage it to improve and change how we work on some aspects of the industry.

Stay tuned as we dig into this subject and try to turn a BIM model into an NFT because why not?

References

- https://www.tradingview.com/symbols/BTCUSD/

- https://www.tradingview.com/symbols/ETHUSD/

- https://dune.com/rchen8/opensea

- https://studio.glassnode.com/metrics?a=ETH&m=transactions.TxTypesBreakdownRelative&resolution=24h

- https://academy.binance.com/en/glossary/block-reward

- https://andersbrownworth.com/blockchain/

- https://academy.binance.com/en/glossary/halving

- https://academy.binance.com/en/articles/proof-of-work-explained

- https://academy.binance.com/en/glossary/proof-of-stake

- https://crypto.com/university/crypto-tokens-vs-coins-difference

- https://academy.binance.com/en/articles/a-guide-to-crypto-collectibles-and-non-fungible-tokens-nfts

- https://ethereum.org/en/developers/docs/standards/tokens/erc-721

- https://boredapeyachtclub.com/

- https://en.wikipedia.org/wiki/Everydays:_the_First_5000_Days

- https://ethereum.org/en/developers/docs/standards/tokens/erc-20/

- https://www.archdaily.com/959011/mars-house-first-digital-home-to-be-sold-on-the-nft-marketplace

- https://www.zaha-hadid.com/design/nftism-at-art-basel-miami-beach/

- https://en.wikipedia.org/wiki/Decentralized_autonomous_organization

- https://www.mckinsey.com/capabilities/mckinsey-digital/our-insights/blockchain-beyond-the-hype-what-is-the-strategic-business-value

- https://www.integrated-projects.com/post/nft-your-building

- https://www.archdaily.com/973936/tallinn-architecture-biennale-announces-first-ever-blockchain-funded-pavilion-as-new-winning-installation

Francisco Maranchello

A proactive entrepreneur at heart who constantly seeks new challenges. As an Architect who codes, I have broadened my skill set through a passion for technology and innovation. I believe technology is the future of architecture and the built world. Always learning and leveraging cutting-edge technologies to seek new answers, I bring a holistic approach when facing new challenges.